Go back

As compute moves off Earth, cybersecurity, geopolitics and supply-chain risks become critical in the race to control the orbital layer. Read more in the op-ed by Tatiana Skydan.

April 2, 2026

On April 1, 2026, NASA launched Artemis II, the first crewed mission to leave Earth orbit since Apollo 17 in 1972. Four astronauts – Reid Wiseman, Victor Glover, Christina Koch and Jeremy Hansen – are currently flying a 10-day trajectory around the Moon aboard the Orion spacecraft, powered by NASA’s Space Launch System (SLS) rocket.

At face value, Artemis II is a milestone in human exploration. At the same time, Blue Origin filed plans for “Project Sunrise” – a proposed constellation of up to 51,600 satellites designed around a radical idea: space-based infrastructure to support the growing compute and bandwidth needs of artificial intelligence.

Put those two events together and a new reality emerges. The next infrastructure race is happening in orbit. And increasingly, there is a cybersecurity aspect in it.

The Artemis program is often framed as a scientific mission. In reality, it is a strategic logistics network for cislunar space.

The architecture includes:

The program involves a wide industrial and geopolitical coalition:

Government agencies

Industrial partners

By the early 2030s, the Artemis ecosystem is projected to exceed $93B in total program cost, spanning launch vehicles, lunar systems, orbital infrastructure and commercial partnerships.

This is not just exploration.

It is the construction of the next strategic layer of infrastructure beyond Earth orbit.

And that layer increasingly intersects with AI, communications networks, and cyber defense.

The narrative around artificial intelligence has largely focused on semiconductors.

But the real constraints are shifting.

The AI economy is now limited by three physical bottlenecks:

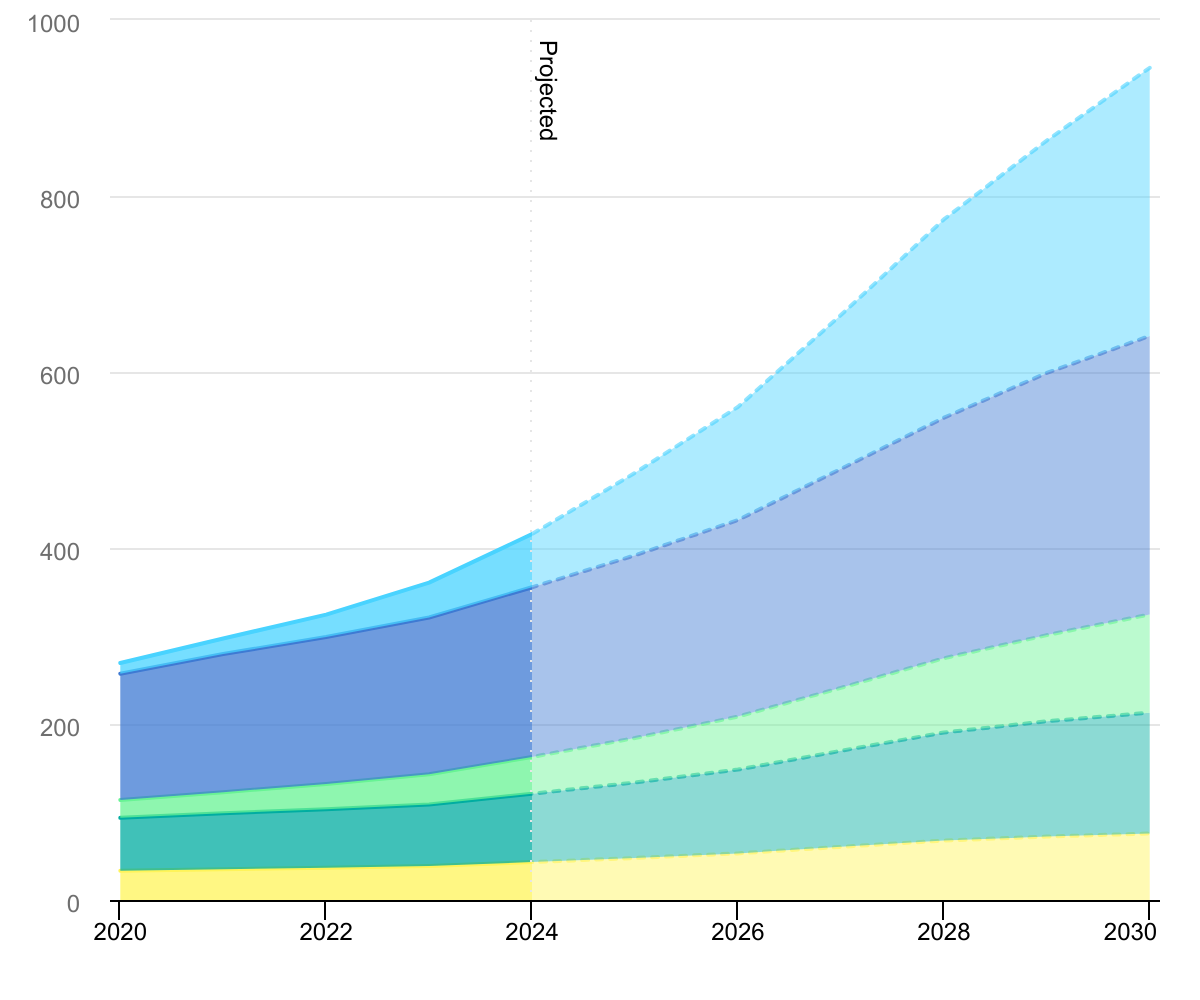

Modern hyperscale data centers typically consume 100 megawatts (MW), with some emerging AI-focused facilities pushing toward 650 MW or higher.

According to the International Energy Agency (IEA) estimates, global data center electricity consumption was approximately 415 TWh in 2024, representing about 1.5% of global power consumption, following a 12% annual growth rate over the past five years.

Driven by AI and accelerated computing, demand is projected to more than double towards 945 TWh by 2030.

At the same time, power grids in the United States and Europe are experiencing severe interconnection delays.

In the U.S. alone, more than 2 terawatts of proposed generation capacity are currently waiting in grid interconnection queues.

The implication is clear: The AI industry is running into hard physical constraints on Earth.

And when infrastructure limits appear, capital starts looking for alternatives.

Blue Origin’s proposed Project Sunrise constellation of up to 51,600 satellites is one such alternative.

The FCC filing describes a system designed around:

The concept overlaps with initiatives from other technology players:

- SpaceX: Starlink, currently the largest satellite network on Earth with more than 5,000 operational satellites

- Amazon: Project Kuiper, a planned broadband constellation of 3,200 satellites

- China: the Guowang constellation, expected to include roughly 13,000 satellites

- Google: Project Suncatcher, exploring solar-powered computing infrastructure in orbit with geospatial company Planet Labs

If Sunrise were built at full scale, it would represent one of the largest distributed computing and communications systems ever constructed.

But the technical story is only half of the equation.

As digital infrastructure moves into orbit, cybersecurity is here to accompany the space strategy.

Satellites are no longer just communications relays. They are network nodes that need to be secure by design.

These categories of threat need to be taken into account:

Older satellites often rely on legacy encryption protocols or limited authentication layers.

Security researchers have repeatedly demonstrated proof-of-concept exploits targeting satellite command channels.

The scale of mega-constellations dramatically expands this attack surface.

Satellite communications already support:

As AI workloads move into distributed space networks, those networks begin to overlap with defense infrastructure. That creates a dual-use reality.

An AI-enabled satellite network might simultaneously carry:

This makes orbital infrastructure more sensitive for cyber espionage and electronic warfare.

Mega-constellations require millions of components:

In 2020, the SolarWinds hack demonstrated how devastating supply-chain compromises can be for software infrastructure.

In space systems, the consequences could include:

The move toward space infrastructure aligns with a broader technological trend: decentralization.

Three different systems are converging:

Instead of a few centralized data centers, the future may involve globally distributed compute nodes spanning:

This architecture is more resilient. But it is also more complex to secure. Cybersecurity will increasingly require autonomous defense systems powered by AI itself. In other words: The same technology driving the AI boom may also be required to defend the infrastructure supporting it.

Space infrastructure has rapidly become a strategic asset class.

Two competing blocs are emerging.

U.S.-aligned ecosystem

China-led ecosystem

Control over orbital networks will shape:

In geopolitical terms, this resembles the historical competition for control over global maritime routes. Except the new trade routes carry data instead of cargo.

For markets, the story is less about science fiction and more about supply chains. Three sectors are likely to benefit regardless of whether orbital data centers arrive in 2028 or 2040.

Satellite constellations and AI clusters both depend on high-speed optical interconnects. Companies exposed to this layer include:

These technologies form the arteries of the AI economy.

Ground infrastructure and satellite communications providers sit at the toll booths of the space economy. Examples include:

AI increases the value of satellite imagery. Companies operating in this sector include:

These platforms increasingly integrate machine learning and real-time analytics for defense, agriculture, climate monitoring, and logistics.

A constellation the size of Project Sunrise will require approval from multiple regulatory bodies:

Expect intense conflicts around:

SpaceX, Amazon and other operators will not passively accept new entrants to orbital infrastructure. This is shaping up to be one of the largest regulatory battles in the history of telecommunications.

The headline story is simple:

Bezos wants to build space-based data centers. But the underlying signal is much larger. The AI revolution is expanding so quickly that it is colliding with the physical limits of Earth’s energy grids and network infrastructure.

Artemis II signals humanity’s return to deep space. Project Sunrise suggests why.

The next generation of infrastructure will not stop at the edge of the atmosphere. And when that infrastructure becomes critical to global communications, artificial intelligence and military command systems, the frontier stops being purely scientific.

It already has become economic, strategic and cybernetic. The next great infrastructure race may not just be about who builds the fastest chips. It may be about who secures the orbital layer of the internet itself.

Governments?

Geopolitical alliances?

Private companies building the next generation of space infrastructure?

Or the hackers and cyber actors who will inevitably target it?

Because once computing, communications and AI extend into orbit, industrialization of near-Earth orbit will become a new arena of competition.

If launch costs continue falling - from about $20,000/kg during the Space Shuttle era to a potential $100-$200/kg with systems like Starship - massive orbital construction could become economically viable.

In that scenario, the internet evolves again: from telegraph cables to fiber networks, to cloud data centers, to satellite constellations - and eventually to orbital computing infrastructure.

So the real question is WHO controls compute, who controls energy and who secures the orbital layer of the internet itself.

Author: Tatiana Skydan, co-founder at THE SIGN

You can support TheSIGN by becoming our SATELLITE. Click to learn more about sponsorship.